In crypto, Aave refers to two connected things: the Aave Protocol, a decentralized lending system, and AAVE, its governance token. Aave is a non-custodial DeFi liquidity protocol that lets you supply crypto to earn interest, borrow crypto against collateral, and interact with lending markets through smart contracts rather than a bank or a centralized company.

The name fits the philosophy: "aave" is Finnish for ghost, the idea being open finance that moves value without a middleman standing in the way. This guide explains what Aave is, how the protocol works, how lending and borrowing function, what the AAVE token does and much more.

Key Takeaways

- Aave refers to both the Aave Protocol, a non-custodial DeFi lending system, and AAVE, the governance token used to help steer the protocol.

- Aave lets users supply crypto to liquidity markets, borrow against collateral, and interact with lending rules enforced by smart contracts rather than a bank or centralized lender.

- Supplying assets on Aave may earn variable interest through aTokens, while borrowing requires over-collateralization and careful monitoring of the Health Factor.

- The Health Factor is the main liquidation-risk gauge: if it falls below 1.0, part of the borrower’s collateral can be sold to repay the loan.

- Aave interest rates are algorithmic and variable, rising or falling based on each market’s utilization and borrowing demand.

- The AAVE token is mainly used for governance, giving holders a role in decisions such as risk parameters, asset listings, and protocol upgrades.

- Aave is known for DeFi-native features such as flash loans, multi-chain liquidity markets, GHO, and newer architecture such as Aave V4’s Hub-and-Spoke model.

- Using Aave removes company-level custody risk but introduces other risks, including smart-contract bugs, liquidation, volatile rates, oracle failures, governance changes, and staking slashing risk.

What Is Aave Crypto?

Aave is a decentralized, non-custodial liquidity protocol that lets users supply crypto, borrow against collateral, and interact with lending markets through smart contracts instead of a bank or centralized crypto company.

In simple terms, users take one of two roles. Suppliers deposit supported crypto assets into shared liquidity markets and may earn interest. Borrowers post collateral and borrow from those markets. The matching, interest accrual, collateral rules, repayments, and withdrawals all run through smart contracts deployed across more than a dozen blockchain networks.

The scale behind that description is easy to miss until you see it charted. Aave is the single largest protocol in on-chain lending, holding roughly $21.7 billion in deposits and commanding about a 36% share of the entire DeFi lending category, as the chart below makes plain.

The word that carries the most weight is non-custodial. With a traditional lender or centralized crypto platform, you hand over your assets and trust the company’s balance sheet, competence, and promises. With Aave, your counterparty is publicly viewable code. Aave Labs, the company that helps write the software, does not custody user funds or operate the markets directly. You verify the smart contract instead of trusting a corporation.

To truly grasp how Aave removes the middleman, it helps to understand the underlying technology driving it. In this MIT lecture on Smart Contracts and DApps, Gary Gensler explains the mechanics of decentralized applications, providing an excellent academic foundation for how protocols like Aave operate securely without human intervention.

The Essential Aave Vocabulary

How Does Aave Work?

Stripped to its essentials, using Aave runs through five steps:

- Connect a Web3 wallet: You reach the Aave interface with a non-custodial wallet like MetaMask or Rabby.

- Supply liquidity: Suppliers deposit supported assets into a market's smart contract and instantly receive yield-bearing aTokens that accrue interest right inside their wallet balance.

- Post over-collateralized assets: Borrowers lock up volatile assets such as ETH or wBTC, which sets a borrowing limit determined by each asset's Loan-to-Value (LTV) ratio.

- Draw out borrowed crypto: Borrowers take stablecoins or other assets from the shared pool at a variable rate, and the position immediately gets a Health Factor.

- Algorithmic rate rebalancing: As capital leaves the pool, the contract nudges interest rates up based on utilization, drawing in new suppliers and keeping the market balanced.

No loan officer reviews an application and there's no waiting period. Anyone with a compatible wallet and supported assets can supply or borrow, subject to each market's rules, and the whole process executes in minutes and stays visible on-chain.

That activity is measurable, and it tells a story. Token Terminal's data puts Aave at roughly 6,600 daily active users against about $9.3 billion in active loans in early 2026. The interesting detail is in the shape of the two lines below: the value of outstanding loans has grown far faster than the raw user count, a sign that larger and more sophisticated players are doing more of the borrowing over time.

%2520vs%2520active%2520loans.webp&w=3840&q=75)

Supplying Crypto on Aave

Supplying means depositing a supported asset into an Aave market, where it becomes liquidity others can borrow. In return you receive an aToken (supplying USDC gives you aUSDC) which represents your deposit and accrues interest directly in your balance over time.

The rate suppliers receive, usually shown as a supply APY, is variable: it tracks borrowing demand and can move up or down at any time. Heavier borrowing demand for an asset generally lifts the rate paid to its suppliers. You can toggle whether a supplied asset also serves as collateral for your own borrowing, and you can withdraw whenever the market has enough free liquidity to cover it. Because rates fluctuate, supplied yield is something you may earn rather than a guaranteed return, and supplying still carries smart-contract, market, and liquidity risk.

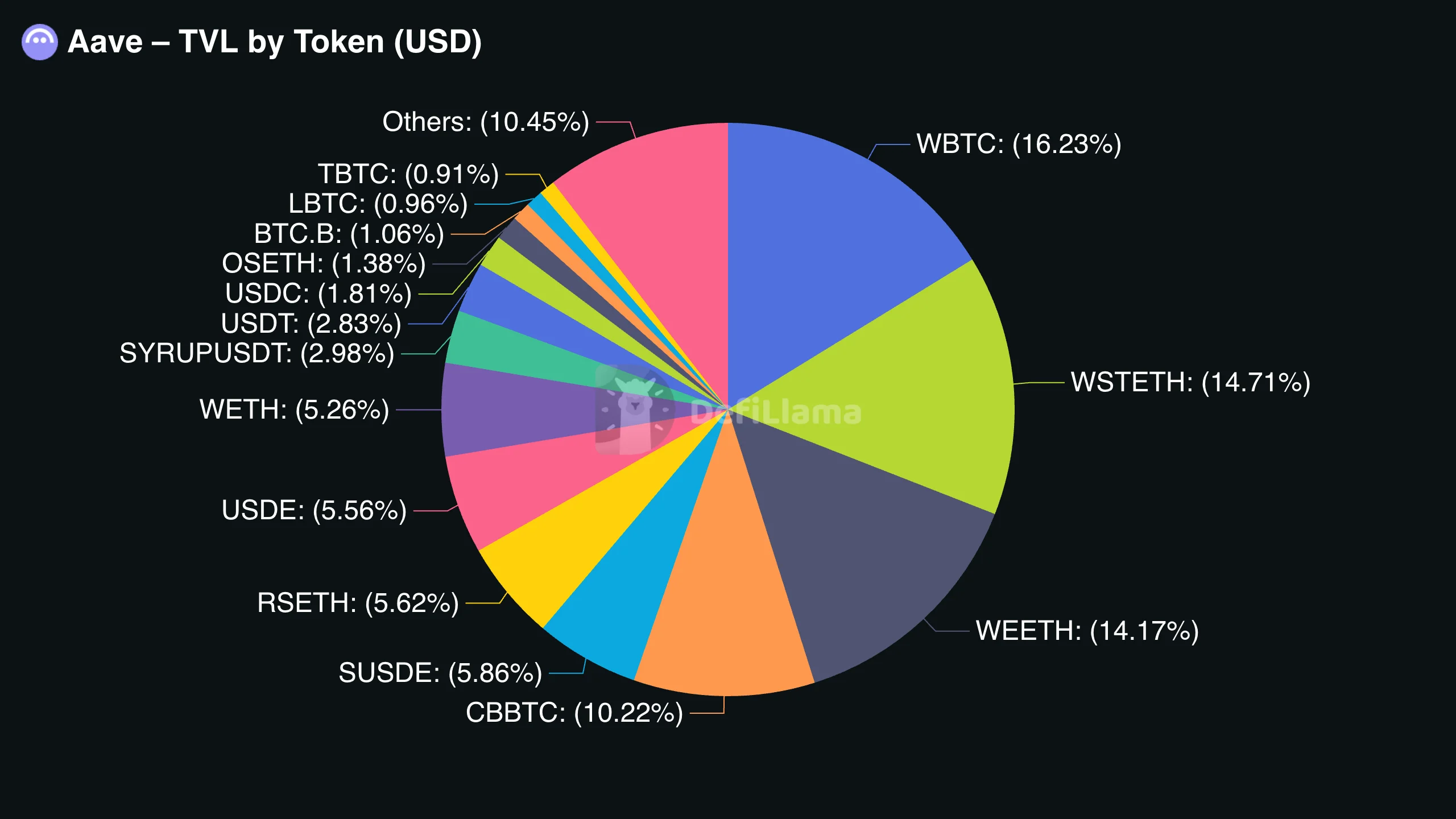

What suppliers actually deposit skews heavily toward stablecoins. Breaking Aave's TVL down by token, as in the chart below, Bitcoin and Ethereum derivatives dominate.

Borrowing Crypto on Aave

Borrowing on Aave means locking up one asset as collateral to borrow another. Aave loans are over-collateralized, so you must post more value than you take out. For instance, supplying $1,000 of ETH to borrow a few hundred dollars of a stablecoin. If that sounds backwards (why borrow against money you already have?), the usual reasons are getting liquidity without selling, avoiding a taxable sale, or adding leverage. Because there's no credit check, the excess collateral is what protects the protocol and its suppliers if a borrower walks away.

In a healthy market, borrowing and repaying stay roughly in balance day to day. The daily comparison below, drawn from Aave V3 on Ethereum, plots borrow volume above the zero line and repayments below it, and the two sides move in near-lockstep. That symmetry is exactly what you'd expect from an active, liquid lending market, rather than the lopsided, one-way rush for the exits that precedes a crisis.

.webp&w=3840&q=75)

The number every borrower watches is the Health Factor, a single figure summarizing how safe a position is. It rises when you add collateral or repay debt, and falls when your collateral loses value or your debt grows. Each asset has a liquidation threshold, and if your Health Factor drops below 1.0, the position becomes eligible for liquidation. Part of your collateral is sold to repay the loan and pull the position back to safety. Liquidation bots watch for exactly this moment, day and night. A falling market can push a position toward that line fast, which is why monitoring the Health Factor is the difference between borrowing and getting liquidated on a quiet Sunday.

Those quiet Sundays are exactly when things go wrong. The chart below overlays ETH's price with aggregate liquidation volume; the tall red spikes mark moments when a sharp price drop cascaded into waves of forced selling across the market. For a borrower whose Health Factor was sitting too close to 1.0, one of those red bars is the moment the bots came calling, and by then it is already over.

Aave Interest Rates and Liquidity Markets

Aave sets interest rates algorithmically, per asset, based on utilization: the share of a market's supplied liquidity currently borrowed. When a market is lightly used, rates stay low to encourage borrowing. As utilization climbs toward a target, rates rise, and past a built-in inflection point they rise sharply, which both discourages further borrowing and rewards suppliers for providing scarce liquidity. This keeps each market balanced with no one setting rates by hand. Both supply and borrow rates are variable, so any figure you see is a snapshot, not a fixed term.

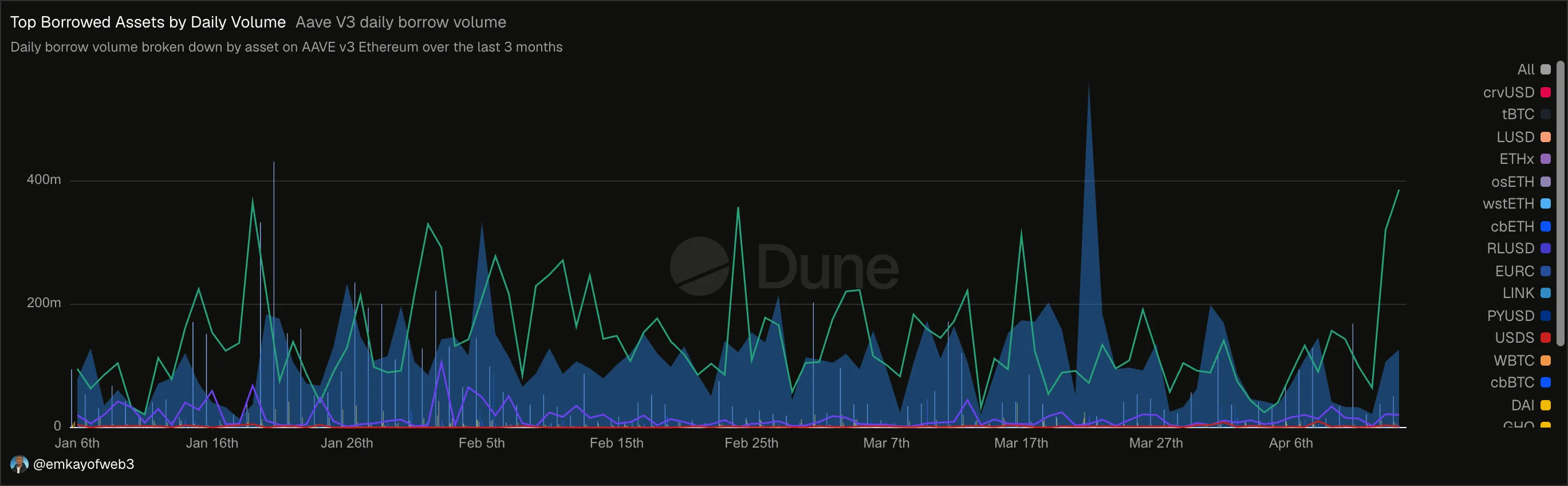

Because rates are set per asset, the mix of what's being borrowed matters. Breaking Aave V3's daily borrow volume down by token, as in the chart below, shows demand rotating across assets. Stablecoins alongside wrapped BTC and ETH variants trade the lead from one day to the next, with total daily borrowing swinging from tens of millions of dollars to well over $400 million. Each of those flows tugs on its own market's utilization, and therefore its rate.

What Is the AAVE Token?

AAVE is the native token at the center of the ecosystem, and its primary job is governance. Holders can propose and vote on Aave Improvement Proposals (AIPs) that decide everything from which assets get listed and what risk parameters apply, to major upgrades like the protocol's architecture. Owning AAVE is effectively a vote on how Aave evolves.

AAVE also plays a role in protocol security. It can be staked to help backstop the protocol against shortfalls, in the form the staking section below describes. Separately, the ecosystem issues GHO, an over-collateralized stablecoin native to the protocol with its own mechanics. One thing this article deliberately skips is price. The AAVE token trades on exchanges and is volatile, but understanding what the token does is a separate matter from any view on what it's worth, and nothing here is a prediction or a recommendation.

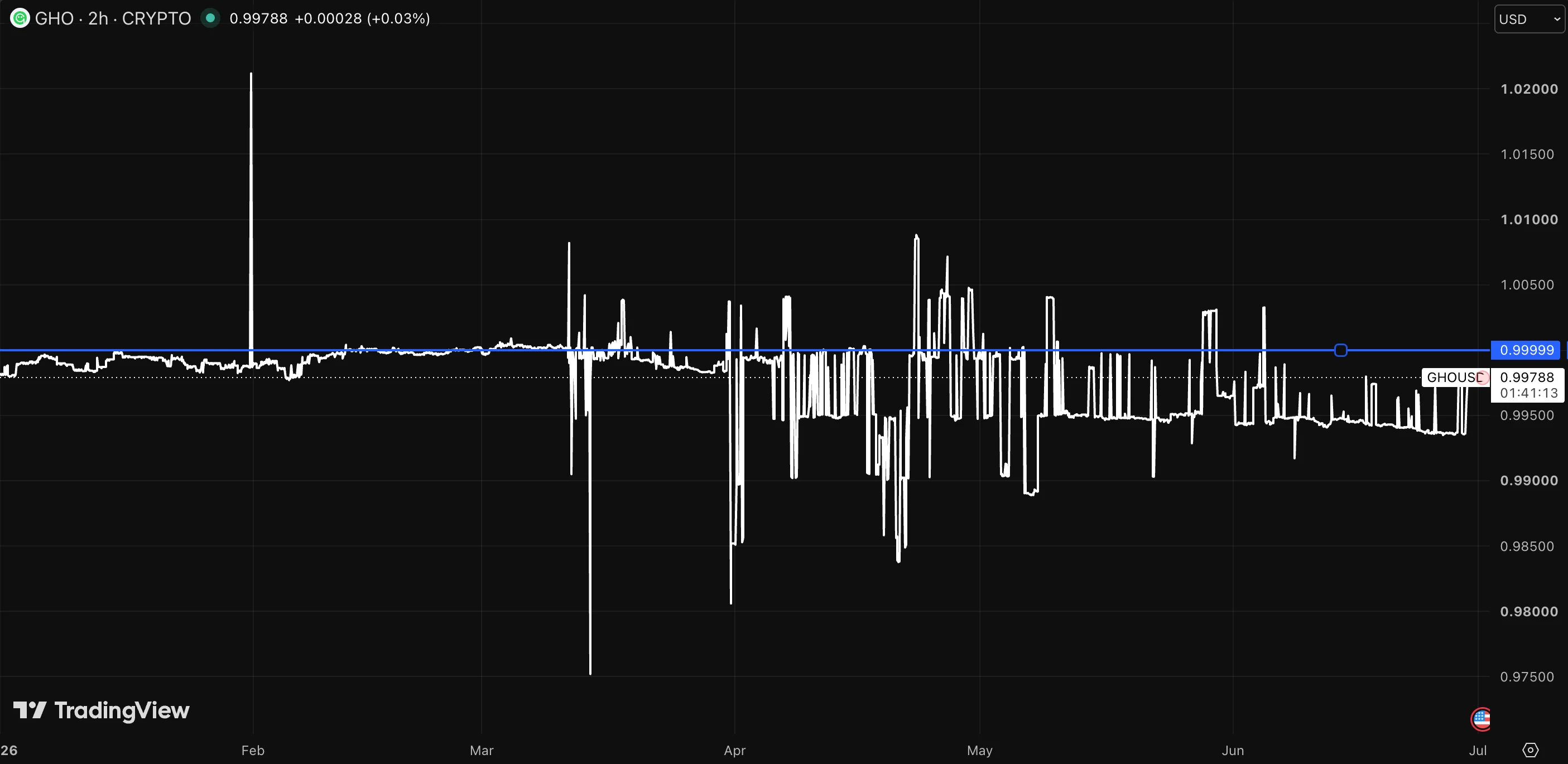

For a stablecoin, the entire job is staying pinned to a dollar, and, as the chart below shows, GHO has largely managed it. The price holds in a tight band just under $1.00 (around $0.998 at the time shown), with only brief spikes and dips before each return to peg. That kind of quiet chart is the flattering one for a stablecoin to have.

Aave V3 and V4

"Creating significant borrow demand... channeling that back into the real economy." | Stani Kulechov, founder of Aave

That line captures the strategic rationale behind Aave's biggest re-architecture to date. Kulechov's argument is that DeFi already has a surplus of supplied liquidity; the protocol's next job is to put it to work by driving borrowing demand and routing capital toward real credit markets.

Aave V3 is the workhorse that made the protocol the largest decentralized lender, holding the majority of its total value locked across more than twenty networks and commanding a majority share of the DeFi lending market. It introduced risk tools such as efficiency mode (E-Mode) for correlated assets, isolation mode for riskier ones, and supply and borrow caps. For most people interacting with Aave today, V3 is the version their funds sit in.

Aave V4 went live on Ethereum mainnet on March 30, 2026, in a deliberately capped, "training wheels" launch. Instead of a separate liquidity pool per market, V4 uses a Hub-and-Spoke model: a central Liquidity Hub holds and accounts for liquidity, while modular Spokes run individual borrowing markets with their own isolated risk settings, all drawing on the shared Hub. (At launch there were three hubs — Prime, Core, and Plus — graded from lower to higher risk.) The goal is to stop liquidity from fragmenting across markets and to let governance add or tune markets without shuffling funds around. V4 also redesigned liquidations to repay only enough debt to restore a position to a target level of safety, rather than penalizing borrowers more than necessary.

Architectural Evolution: Aave V3 vs Aave V4

V4 deploys alongside V3 rather than replacing it overnight, so users migrate on their own timeline, and the mechanics of supplying, borrowing, collateral, and the Health Factor stay conceptually the same across both.

What Are Flash Loans on Aave?

A flash loan is a loan borrowed and repaid within a single blockchain transaction. There's no upfront collateral, because the protocol enforces one strict rule: if the borrowed amount plus a fee isn't returned by the end of that one transaction, the entire transaction reverts as if it never happened. The loan completes fully or doesn't occur at all.

That atomic structure makes flash loans a developer's tool rather than something most people tap through a simple interface. Their legitimate uses include arbitrage between markets, refinancing a loan from one protocol to another, and swapping the collateral behind a position, all executed automatically inside one transaction. Aave helped popularize them and is closely associated with the feature. They have a Jekyll-and-Hyde reputation, though: the same mechanism has been turned against poorly designed protocols in some of DeFi's larger exploits, which is why flash loans are best understood by those building on top of Aave rather than experimented with casually.

Aave Staking, Safety Module, and Umbrella

Aave has long let users stake to help secure the protocol, and that system was overhauled in 2025. Historically, the Safety Module let people stake AAVE (as stkAAVE) and AAVE/ETH Balancer pool tokens as a backstop; if the protocol suffered a shortfall, those staked assets could in theory be "slashed" to cover it.

On June 5, 2025, Aave activated Umbrella, an upgraded safety system that changed the mechanics. Instead of relying on a governance vote, Umbrella slashes automatically and in real time when bad debt in a specific asset exceeds a preset buffer. Users now stake interest-bearing aTokens (such as aUSDC, aUSDT, and aWETH) or GHO into per-asset vaults, keep earning their underlying yield, and receive additional "Safety Incentive" rewards for accepting slashing risk. Crucially, that risk is isolated: staking aUSDC only ever helps cover a USDC shortfall, never losses elsewhere, and each vault has a deficit offset, so the Aave treasury absorbs the first slice of any bad debt before stakers are touched. Unstaking runs through a cooldown (20 days) and a short withdrawal window (2 days).

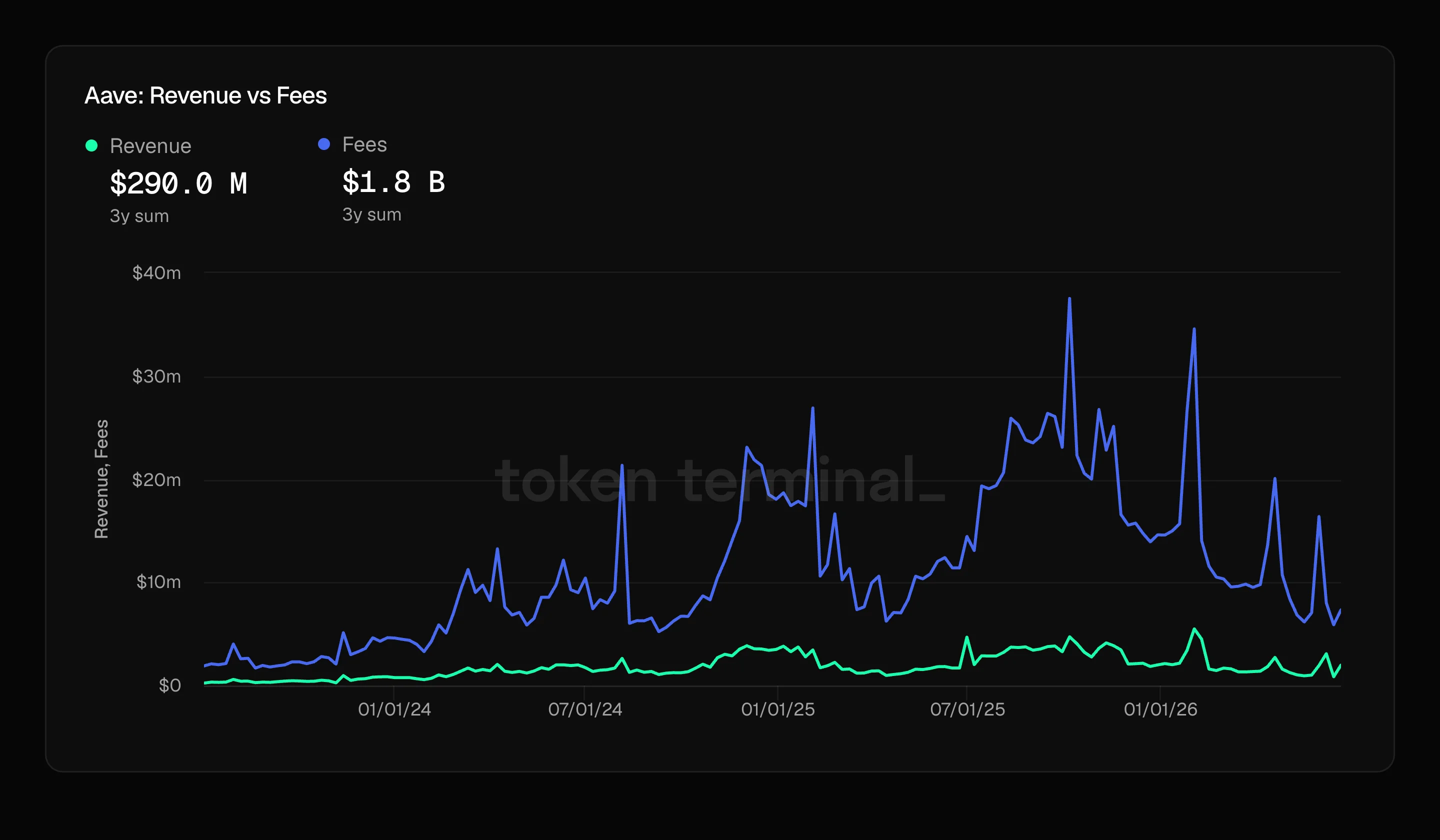

That treasury backstop is credible only because the protocol earns real money. Over roughly three years Aave has generated about $1.8 billion in total fees paid by borrowers, of which around $290 million became protocol revenue. The chart below shows how spiky those fees are, jumping with bursts of market activity, against the far steadier revenue line that ultimately funds the safety system and the deficit offsets behind it.

As part of the transition, the legacy stkAAVE position stays active but with slashing disabled, serving mainly as governance power, while staked GHO was migrated toward a savings version (sGHO) alongside an optional higher-risk Umbrella vault. The essential point for anyone considering it: Aave staking is not risk-free. In exchange for rewards, you accept that your staked assets can be reduced to cover a protocol shortfall, and slashed assets are not recoverable.

Aave Risks: Liquidations, Smart Contracts, and Market Volatility

Using Aave means taking on several distinct risks, and understanding them matters more than chasing any rate.

Smart contracts trade away some risks of trusting a company and introduce others. DeFi protocols, Aave included, have lived through bad-debt and exploit events, and a backstop like Umbrella covers shortfalls only up to its funded limits.

Aave vs Centralized Crypto Lending

The clearest way to place Aave is against a centralized crypto lender, where a company takes custody of your assets and runs the lending itself.

Neither model is universally safer; they fail in opposite directions, which the matrix below lays bare.

The Doomsday Matrix: Aave vs a Centralized Crypto Lender

That left column isn't only theory either. When Celsius froze withdrawals in 2022 and later filed for bankruptcy, followed by BlockFi after the FTX collapse, users learned the hard way that "earning yield" with a centralized lender meant lending their coins to a company they couldn't audit. A centralized lender offers familiar accounts and a support line but asks you to trust its solvency and custody. Aave removes that company-level counterparty and hands you the full responsibility for security, monitoring, and understanding the mechanics.

Aave vs Compound

Aave and Compound are both established DeFi lending protocols built on the same core idea: supply assets to earn yield, borrow against over-collateralized positions. The differences are mostly scope and features.

Aave is generally the larger of the two and is known for flash loans, deployments across many networks, its GHO stablecoin, and successive architecture upgrades. Compound runs its own markets, governance, and interest-rate model. For most beginners, the more useful takeaway is that the two share the same fundamental design rather than the specifics that separate them.

How to Use Aave Safely

DeFi lending offers real financial autonomy and zero hand-holding. Protect your capital by treating these five rules as non-negotiable.

- Treat the APY as a moving target: Never build a budget around an advertised 12% supply or borrow rate. Aave's rates are dynamic and utilization-driven; a sudden rush of borrowing can spike a borrow rate well into the double digits overnight.

- Keep a "sleep well at night" Health Factor buffer: Don't let a borrowing position hover near 1.1. Aim for a baseline around 1.5 to 2.0 so a violent weekend flash-crash doesn't hand your collateral to a liquidation bot.

- Don't loop leverage blindly: "Folding" strategies that repeatedly supply ETH, borrow stablecoins, buy more ETH, and re-supply tighten your liquidation window with each turn, converting a modest correction into a full wipeout.

- Read the Umbrella staking fine print: If you chase higher yields by staking aUSDC or GHO into the safety system, remember you're acting as the protocol's insurer: if it suffers unrecoverable bad debt in that asset, your staked principal can be slashed and won't come back.

- Verify contract addresses independently: Scammers deploy pixel-perfect clones of the Aave front-end to drain wallets. Bookmark the official URL and check the router contract address on an independent block explorer before approving any token spending.

Closing Thoughts

Aave is one of DeFi’s most important lending protocols because it lets users supply assets, borrow against collateral, and interact with liquidity markets without handing funds to a centralized lender. The protocol replaces account approvals and company custody with smart contracts, algorithmic rates, governance, and transparent on-chain rules.

That design gives users more control, but it does not remove risk. Borrowers need to understand collateral, Health Factor, liquidation thresholds, variable rates, and market volatility. Suppliers and stakers also face smart-contract risk, liquidity risk, oracle risk, governance changes, network risk, and, in Umbrella vaults, possible slashing.

The safest way to approach Aave is to treat it as powerful but unforgiving infrastructure. Use small positions while learning, keep wide collateral buffers, verify contracts, avoid blind leverage, and remember that DeFi removes the middleman.