In crypto, Compound Finance is a decentralized lending protocol that lets people supply and borrow digital assets through smart contracts. There's no banker, no branch, and no one deciding who qualifies. Interest rates set themselves on-chain based on supply and demand, and the code handles the lending, the borrowing, and the collateral.

Compound was one of the protocols that defined decentralized finance and helped popularize the idea of an algorithmic money market. Below: what Compound Finance is, how the protocol works, how supplying and borrowing function, what the COMP token does, how the current Compound v3 design works, and the risks worth understanding before you go near it.

Key Takeaways

- Compound Finance is a decentralized lending protocol that lets users supply and borrow crypto through smart contracts instead of a bank or centralized lender.

- Suppliers deposit supported assets into Compound markets and may earn variable interest based on borrowing demand.

- Borrowers post collateral and borrow a market's base asset, with loans kept over-collateralized to protect the protocol.

- Compound v3, also called Compound III or Comet, uses a single borrowable base asset per market to isolate risk more clearly than the older pooled model.

- Interest rates on Compound are algorithmic and variable, rising or falling based on utilization and market demand.

- COMP is Compound's governance token, giving holders and delegates the ability to vote on markets, risk parameters, rewards, and protocol upgrades.

- Compound removes company-level custody risk, but it introduces DeFi risks such as smart-contract bugs, liquidation, oracle errors, volatile rates, governance changes, and user mistakes.

- The safest way to use Compound is to treat APYs as moving targets, keep a wide collateral buffer, verify contract addresses, and avoid leverage strategies you do not fully understand.

What Is Compound Finance?

Compound Finance is a decentralized, autonomous interest-rate protocol built on Ethereum and compatible networks. It launched in 2018, founded by Robert Leshner and Geoffrey Hayes, and lets anyone with a crypto wallet supply supported assets to earn interest or post collateral to borrow against. No application, no credit check, no loan officer. The rules live in smart contracts and apply to everyone equally, Leshner has described the protocol as nothing more than "a series of essentially computer programs" that anyone can inspect.

That's the whole pitch. Work that a traditional lender does with compliance teams, risk desks, and underwriters (pricing loans, checking collateral, calling in bad debt) runs here as open code. People often call this an algorithmic money market: a place for short-term lending and borrowing at market-driven rates, except the rates are set by software responding to how much of each market's liquidity is being borrowed, and the whole system is auditable by anyone. No company holds your funds. That combination is what makes Compound a DeFi protocol rather than a crypto lending business.

What Is the Compound Protocol?

The Compound Protocol is the set of smart contracts that run these markets. Suppliers deposit assets, borrowers post collateral and take loans, interest accrues automatically, and anyone can repay or withdraw under the protocol's rules. Changing those rules requires passing on-chain governance, and the contracts have been audited by multiple independent security firms.

How Does Compound Finance Work?

Compound runs on a supply-and-borrow loop, with code where the loan officer used to sit:

- Suppliers deposit a supported asset, adding liquidity to a market.

- Borrowers post collateral and borrow the market's main asset against it.

- Borrowers pay interest, which flows to suppliers as yield.

- Interest rates adjust automatically based on how much liquidity is borrowed.

- Borrowers must keep enough collateral relative to their loan, or the position can be liquidated.

The process is permissionless and near-instant. Anyone with a compatible wallet and supported assets can take part, every position is visible on-chain, and nobody approves you. The catch is the same as the appeal: there's no company to call when something goes wrong. Understanding the rules and managing the risk is on you.

Supplying Crypto on Compound

Supplying means depositing a supported asset into a Compound market. In the current version of the protocol, you earn interest by supplying the market's base asset, typically a stablecoin like USDC, or an asset like ETH. In return you get a position that accrues interest, and you can withdraw whenever the market has enough free liquidity.

The supply rate is variable. It rises and falls with utilization, the share of the supplied base asset currently borrowed, so a market in heavy demand pays suppliers more and a quiet one pays less. Because the rate moves continuously, supplying offers yield you may earn rather than a fixed return, and it still carries smart-contract, market, and liquidity risk. One quirk of Compound's current design: assets posted purely as collateral generally earn no supply interest. Only the base asset does.

Borrowing Crypto on Compound

Borrowing on Compound means posting collateral and borrowing a market's base asset against it. Think of it as a programmable pawnshop: you leave something worth more than you take out. Loans are over-collateralized, so you supply more value in collateral than you borrow, and that surplus is what protects suppliers if a borrower can't repay.

How much you can borrow is set by each collateral asset's collateral factor. An 85% collateral factor means you can borrow up to 85% of the dollar value of that collateral in the base asset. Compound separates this from a higher liquidation collateral factor, the point at which the position becomes eligible for liquidation. The gap between the two is a buffer: you can borrow up to the lower limit, and your collateral isn't at immediate risk until its value falls far enough to cross the higher line. If it does, part of your collateral can be sold to repay the loan and pull the position back to safety. Borrowers repay the base asset plus accrued interest whenever they choose and reclaim their collateral once the debt clears.

The buffer is thinner than it looks, which is why the single most useful borrowing habit is leaving plenty of room below your limit.

Parameters shown are illustrative; Compound's live collateral and liquidation factors vary by asset and network and are set by governance. The lesson is structural: maxing out your borrow leaves almost no cushion.

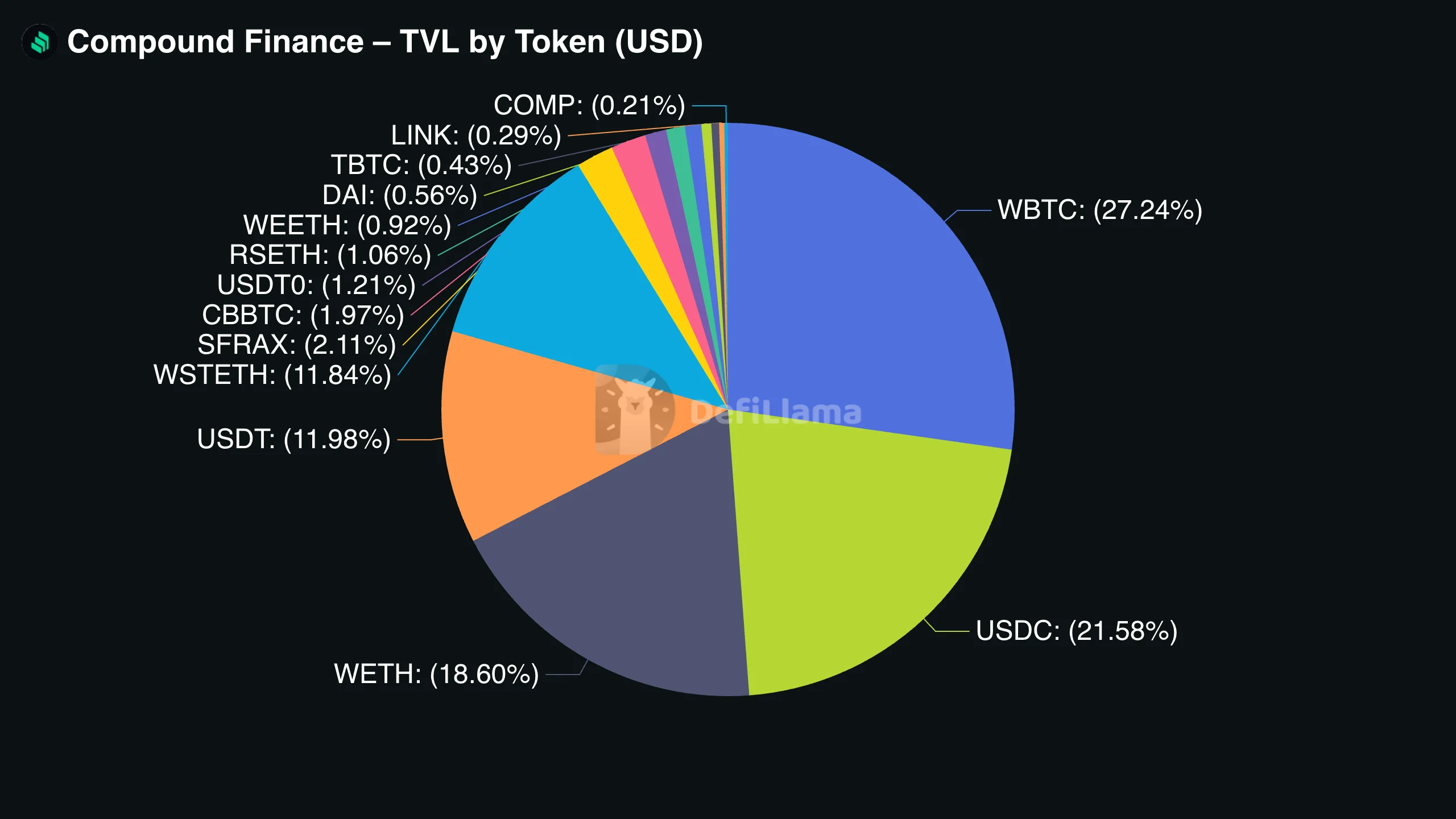

It also helps to know what actually backs these loans in aggregate. The breakdown below shows how Compound's posted collateral is distributed across supported assets. Concentrated, as you'd expect, in a handful of majors like ETH and wBTC, which is worth keeping in mind because the whole market's health leans on the price behavior of a few large collateral types.

Compound v3 / Compound III Explained

Compound has gone through several versions; the current one is Compound v3, also called Compound III and codenamed Comet. Released in 2022, it reorganized the protocol around a simpler, safer design. Instead of one large shared pool where many assets can be borrowed, each Comet market has a single borrowable base asset (such as USDC, ETH, or USDT) plus a defined list of assets you can post as collateral. Comet runs on Ethereum and a range of Layer 2 and EVM-compatible networks, which lowers transaction costs on those chains.

The reason for the redesign is worth hearing from the founder. Announcing Compound III, Leshner described the rationale plainly:

"The most profound change was to move away from a pooled-risk model… A single bad asset (or oracle update) can drain all assets from the protocol. Instead, each deployment of Compound III features a single borrowable asset. When you supply collateral, it remains your property." | Robert Leshner, Compound III is Live (2022)

That single-base-asset model is the defining change. Isolating one borrowable asset per market contains a problem with one collateral type instead of letting it spill across the whole protocol. The trade-off is less flexibility than the old multi-asset design. Compound v2 is being wound down, in late 2025 the Compound DAO voted to pause new borrowing on v2 markets and steer users toward Comet, so v3 is where active lending and borrowing now happen.

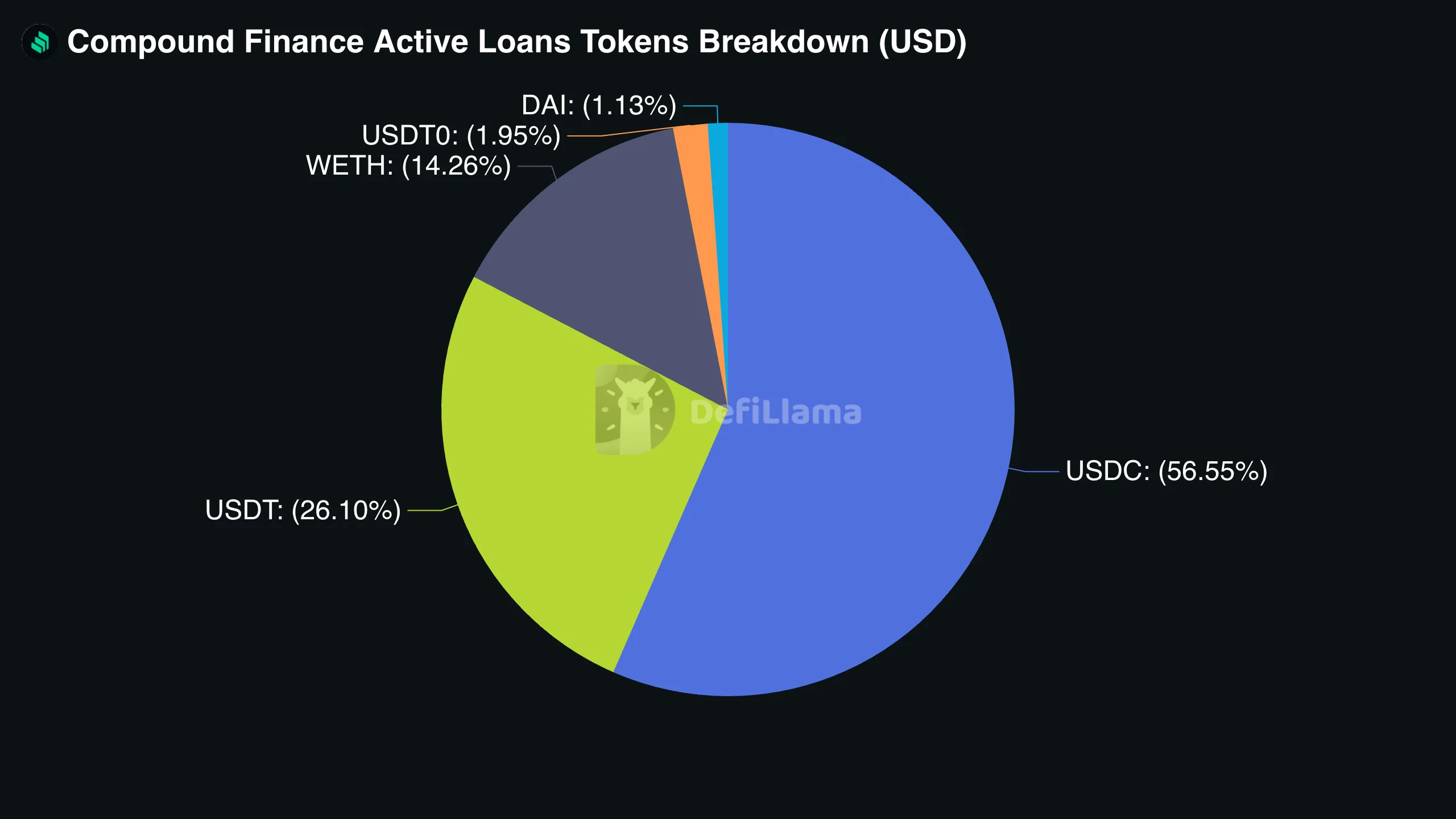

You can see the base-asset design play out in what people actually borrow. Borrowing on Compound is overwhelmingly a stablecoin story: as the breakdown below shows, USDC alone accounts for well over half of active loans, with USDT the next largest. Together with the smaller stablecoins and WETH, dollar-pegged assets make up the vast majority of the borrow book.

How Compound Interest Rates Work

Compound's rates are algorithmic and variable, set by the protocol rather than negotiated. They key off utilization: as more of a market's base asset gets borrowed, borrow rates rise to reward suppliers and cool demand, and they ease when utilization falls. In the current design, supply and borrow rates sit on separate curves rather than being locked together, which gives governance more control over keeping each market stable.

There's a second layer to watch. Compound markets can also distribute COMP token rewards to suppliers, borrowers, or both, at rates governance sets. A headline yield often blends the base interest rate with a COMP incentive, and the incentive portion moves with COMP's price. So a quoted APY on Compound is a moving figure, closer to a weather forecast than a fixed savings rate, and part of it may depend on token rewards that can change.

What Is the COMP Token?

COMP is Compound's governance token, an ERC-20 asset that hands the community control of the protocol. Its job is governance, not payment or yield: holding COMP confers the right to vote on how Compound runs. It's also the token that markets distribute as the incentive rewards described above.

COMP has a bit of history attached to it. When Compound began distributing the token in June 2020, it kicked off the liquidity-mining craze that became known as "DeFi Summer," a stretch where yield-chasing capital flooded into protocols almost overnight. The pace of that distribution has shifted a great deal since. The chart below tracks COMP's distribution rate over time, showing how emissions have tapered from those early liquidity-mining highs as governance has dialed the incentive budget up and down.

Compound Governance

Compound governance is how the protocol changes. COMP holders and their delegates, addresses that holders assign their voting power to, can propose changes, debate them, and vote. Approved proposals run through a governance contract and a timelock that enforces a delay before anything takes effect.

Governance controls the levers that matter: which markets and collateral assets are supported, the collateral factors and other risk parameters, the COMP reward rates, and protocol upgrades. It can also assign a Pause Guardian, a role that can quickly freeze certain functions in an emergency. This is what "decentralized" means in practice for Compound. There's no wizard behind the curtain who can rewrite the rules alone, though a sufficiently coordinated group of token holders can.

Compound Risks: Liquidation, Smart Contracts, and Market Volatility

Using Compound means accepting several distinct risks, and understanding them matters more than chasing a rate. DeFi runs around the clock in an openly adversarial environment. Gauntlet, the firm that has modeled risk for Compound, describes its work as "continuously simulating adversarial behavior" against the protocol, precisely because crypto's volatility stress-tests automated risk parameters in ways a quiet savings product never faces.

Liquidation is not a hypothetical corner case. It's a live, automated process that fires whenever collateral values fall through their thresholds. The chart below tracks the value of liquidations on Compound over time, and the spikes line up neatly with sharp market drawdowns: when prices gap down fast, the liquidation bots do the most work.

Moving from a company to smart contracts removes some risks and introduces others. Compound's code has been audited by multiple firms, it runs a bug bounty, and the DAO has set aside an emergency reserve, but no protocol is risk-free, and a reserve is not deposit insurance. DeFi lending markets, Compound included, have had to respond to exploits and oracle problems, sometimes by pausing affected markets through governance. Audits reduce risk; they don't eliminate it.

Compound Finance by the Numbers

Mechanics aside, it helps to see where Compound actually stands as a business. The figures below are drawn from Token Terminal and DefiLlama, and together they sketch a protocol that is smaller and quieter than at its 2021 peak, but still processing real volume.

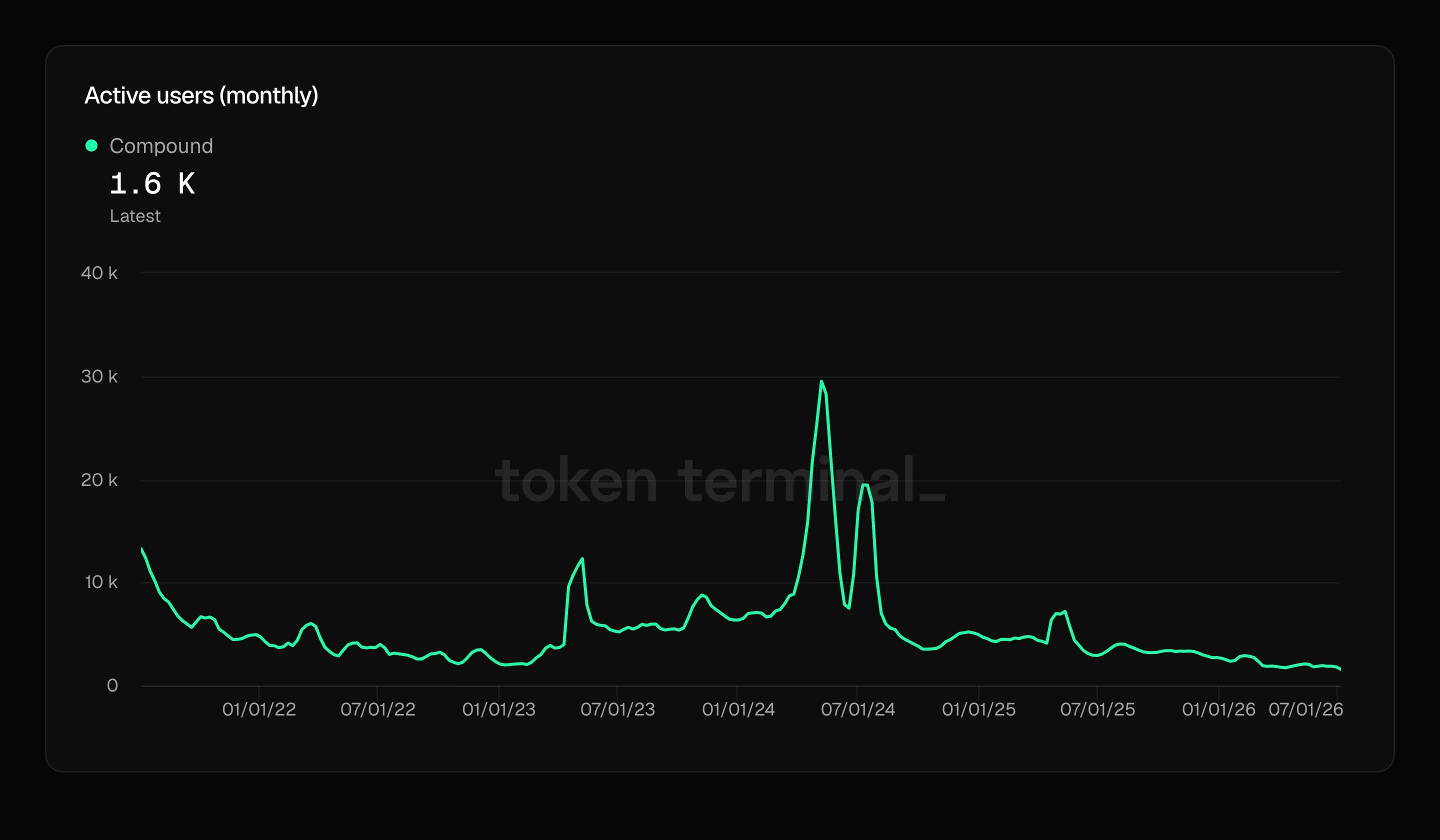

Start with the people using it. Compound's monthly active users have come well off their earlier highs, the latest reading sits around 1,600, down from spikes near 30,000 in mid-2024 and a first surge above 13,000 back in 2021. Activity comes in bursts tied to market events rather than a steady climb.

That activity still generates income for the protocol. Compound's protocol revenue, the slice of borrower interest the protocol keeps after paying suppliers, adds up to roughly $49 million over five years, but it's heavily front-loaded: the tallest bars belong to the 2021 boom, with smaller revivals in 2024, 2025 and early 2026.

.webp&w=3840&q=75)

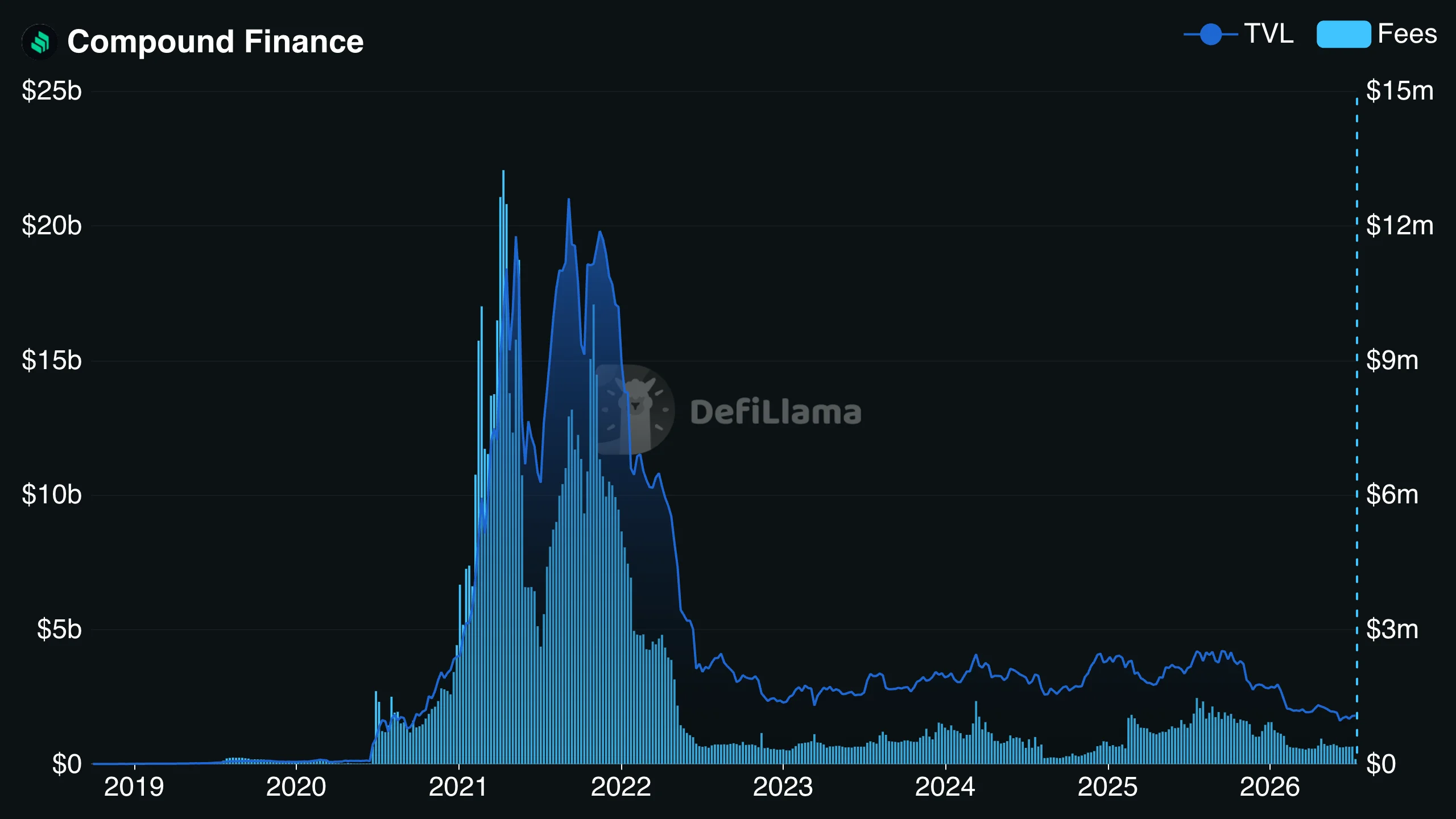

Zoom out to deposits and total fees, and the same shape appears. Total value locked crested above $20 billion in 2021 before settling into the low single-digit billions, and the fees the protocol earns have tracked that rise and fall closely.

Pulled into a single ledger, the year-by-year financials tell the fuller story. Total value locked around $1.9 billion and active loans near $628 million in 2026, fees of about $12 million against modest revenue, and a treasury that has drawn down substantially from its peak.

.webp&w=3840&q=75)

Compound vs Aave

Compound and Aave are the two best-known DeFi lending protocols, and they share a core idea: supply assets to earn yield, borrow against over-collateralized positions, and let algorithms set the rates. Compound helped invent the algorithmic money market and now centers on the streamlined, single-base-asset Comet design. Aave has grown into the larger of the two by total value locked, with a broader feature set including flash loans, deployments across more networks, and its own GHO stablecoin.

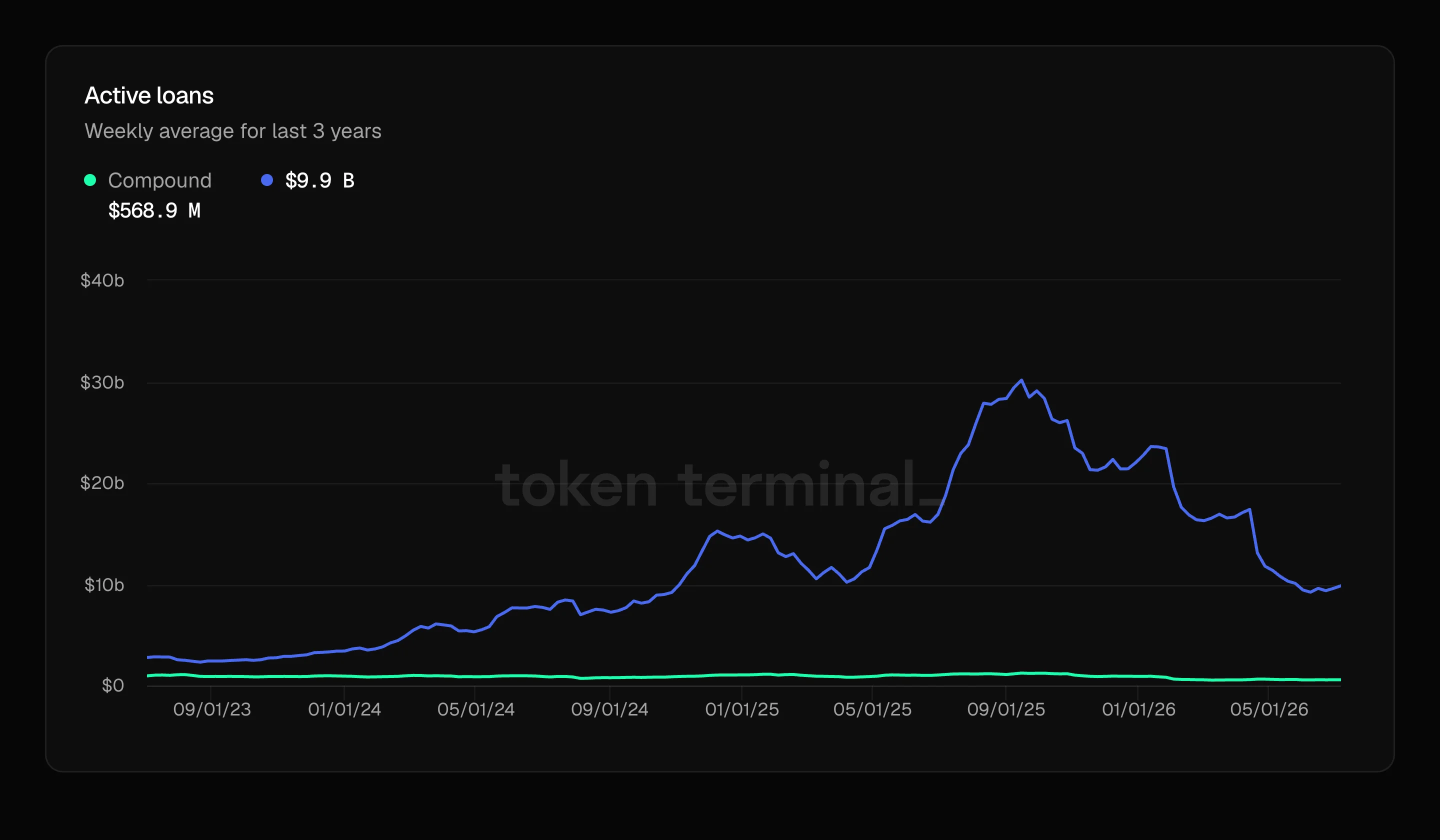

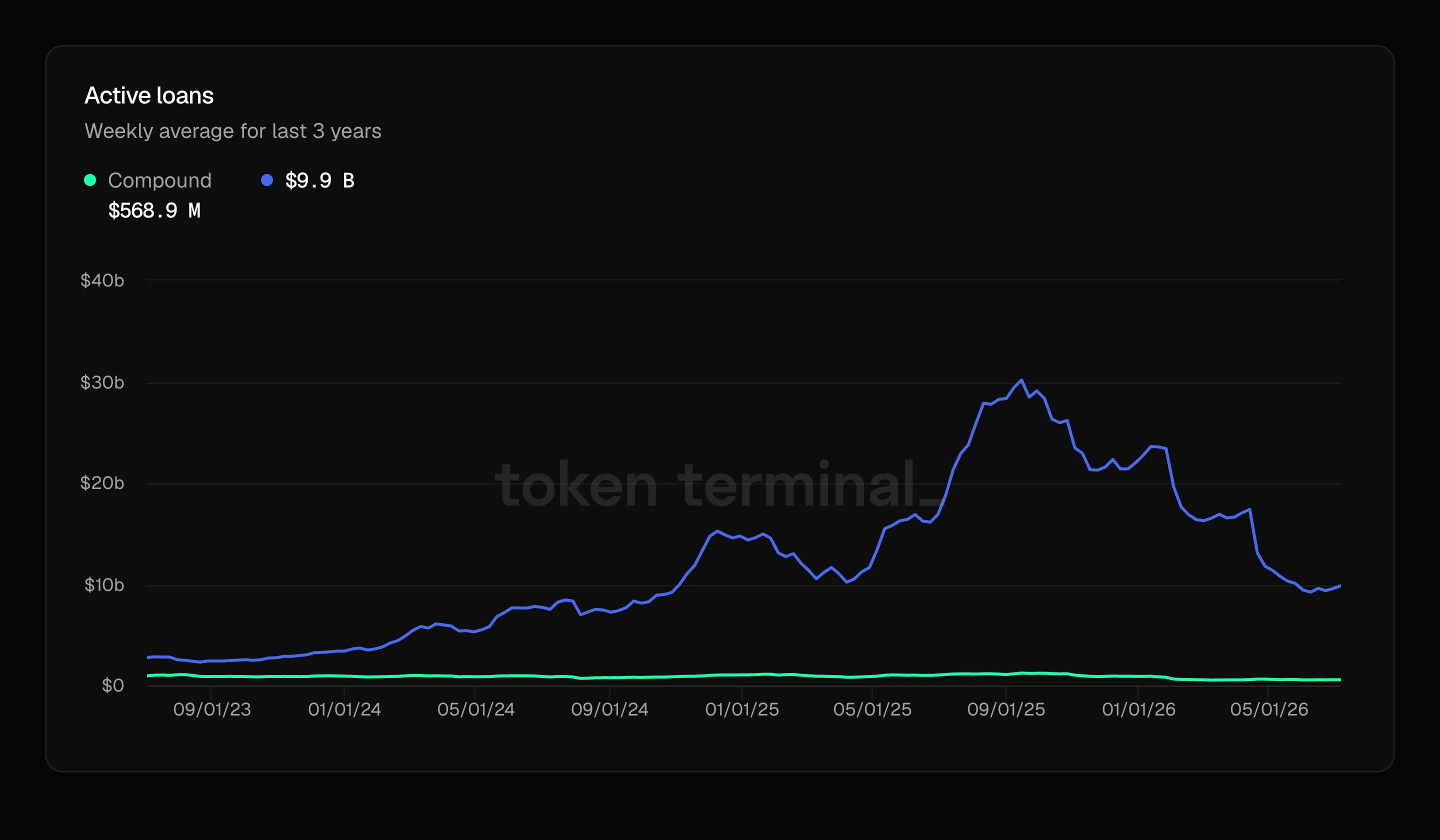

Just how large is that gap? On active loans, Aave dwarfs Compound. The chart below puts them side by side: Aave's active loans swelled toward $30 billion before easing back to around $9.9 billion, while Compound's line barely lifts off the floor at roughly $569 million.

Size isn't the whole story, though. Measured per user, Compound actually earns more than its bigger rival, a recent average revenue per user (ARPU) of about $34 versus Aave's $20, which hints that Compound's smaller base skews toward larger or more active positions rather than casual depositors.

For most beginners, the useful takeaway is that the two run on the same fundamentals. The differences are scope and design philosophy, not the basics of how lending works.

Compound vs Centralized Crypto Lending

It helps to set Compound against a centralized crypto lender, where a company takes custody of your assets and runs the lending itself. The same contrast holds against a traditional bank, and laid side by side, the trade-offs get blunt.

Compound removes the company-level counterparty, there's no firm whose insolvency can freeze your funds, but it loads the full weight of security, monitoring, and understanding the mechanics onto you. Neither model is universally safer. They relocate the risk.

How to Use Compound Safely

DeFi lending eliminates the middleman, and with it the safety net. Protect your capital by treating these five rules as non-negotiable.

- Treat the APY as a moving target: Never build a long-term budget around an advertised supply rate. A surge in liquidity can crush an 8% APY toward 1% with no warning, and rates boosted by token rewards move with the token's price.

- Respect the safety buffer: Never borrow up to your maximum collateral factor. If the limit is 70%, borrowing 30–40% means a violent weekend flash crash doesn't instantly hand your collateral to the liquidation bots.

- Audit the specific network deployment: Compound III runs on Ethereum, Arbitrum, Base, Polygon, and others. Don't assume they share the same risk, Layer 2s carry distinct sequencer, bridge, and liquidity considerations that Ethereum mainnet does not.

- Never loop leverage blindly: Recursive "folding" (deposit ETH, borrow USDC, buy more ETH, re-supply) tightens your liquidation window with every loop, turning an ordinary 15% correction into a wipeout.

- Verify contract addresses independently: Scammers deploy pixel-perfect clones of the Compound front end to drain wallets. Bookmark the official site, and confirm the contract you're approving before you sign anything.

Rule 3 is easy to underrate until you see it. "Compound" is the same protocol deployed across several chains, each holding a different amount of liquidity and carrying its own risks. The chart below shows how Compound's total value locked splits by network, a reminder to check which deployment you're actually using before you supply or borrow.

A useful mental model for the bots in rule 2: liquidation is automated and unsentimental. The code doesn't take weekends, can't be reasoned with, and won't accept "the market will bounce back" as collateral.

Closing Thoughts

Compound Finance helped define DeFi lending by replacing traditional loan desks with smart contracts, collateral rules, algorithmic interest rates, and on-chain governance. Users can supply assets, borrow against collateral, and interact directly with markets, but that openness comes with responsibility.

The most important things to understand are how Compound v3 markets are structured, which asset is borrowable, what collateral rules apply, how variable rates move, and where liquidation risk begins. COMP gives holders a role in governance, but it does not make the protocol risk-free or turn yield into a guaranteed return.

Compound can be a powerful DeFi tool, but it should be approached carefully. Smart-contract risk, oracle risk, governance changes, liquidity limits, volatile collateral, and user error all matter, so safer use starts with small positions, large collateral buffers, verified contracts, and a clear understanding of the market before supplying or borrowing.