A centralized exchange, or CEX, is a company-operated platform where you buy, sell, and trade cryptocurrency through an account. It's how most people first step into crypto: you deposit money, the exchange holds it, you place orders, and the platform matches buyers with sellers.

Picture a bank account you can open in five minutes from your couch, with all the convenience that implies, and none of the two centuries of deposit insurance standing behind a real one. While your crypto sits on a CEX, the exchange controls it, and you're trusting the company's security, solvency, and willingness to honor your withdrawal.

A CEX is one of the two main kinds of crypto exchange. The other is a decentralized exchange, or DEX, where people trade directly from their own wallets through smart contracts, with no company holding their funds. Understanding the gap between them, and between an exchange and a wallet, is the difference between using crypto safely and learning the expensive way.

Key Takeaways

- A centralized exchange (CEX) is a company-operated crypto trading platform where you buy, sell, trade, deposit, and withdraw crypto through an account.

- Most CEXs are custodial: the exchange controls the private keys, so your balance is a claim on the company rather than crypto you directly hold.

- CEX trades usually settle on the exchange's internal ledger; only deposits and withdrawals move on-chain.

- CEXs are easier for beginners than DEXs, offering fiat payments, deep liquidity, order books, and customer support, in exchange for trust.

- The core risks are custody, counterparty and hack risk, withdrawal freezes, insolvency, outages, KYC privacy trade-offs, and regulatory restrictions.

- Proof of reserves improves transparency but doesn't prove solvency unless liabilities are shown and independently checked.

- A CEX works best as a trading and fiat on-ramp tool; long-term holdings are safer in self-custody.

What Is a CEX in Crypto?

A centralized exchange is a company that runs a crypto trading platform, letting users buy, sell, trade, deposit, and withdraw cryptocurrencies through an account. "Centralized" means a single operator runs everything: it holds the funds, maintains the order book, verifies identities, and provides support. This is the model behind most of the large, well-known crypto apps.

It helps to picture the scale of what these companies sit in front of. As the chart below shows, the total crypto market has swung between roughly $1 trillion and more than $4 trillion in the space of three years, and a CEX is the doorway most people walk through to reach any of it.

The trade-off is the thing to grasp early. A CEX is usually far easier to use than a DEX: accounts, passwords, support, and paying with a bank card all feel familiar. In return, you trust the operator to safeguard your assets, run the platform honestly, and let you withdraw when you ask.

How Does a Centralized Exchange Work?

Behind a single "buy" button, a CEX runs a sequence that resembles a traditional brokerage more than a blockchain:

- You create an account with an email or phone number and set up security.

- You verify your identity through KYC, depending on the exchange and your region.

- You deposit funds. Fiat by bank transfer or card, or crypto sent to an exchange-provided address.

- The exchange credits your account balance, an internal record of what you hold on the platform.

- You place an order, choosing a type such as a market order (fill now at the going price) or a limit order (fill only at a price you set).

- The matching engine pairs your order with a compatible one from another user.

- The trade settles inside the exchange, updating both balances.

- You keep the funds on the platform or withdraw them to a bank or an external wallet.

A subtle but crucial mechanic sits in step six. When you trade on a CEX, the transaction usually never touches the blockchain. The exchange records the change on its own internal ledger, the way a bank updates balances without trucking cash between vaults. Only deposits and withdrawals are real on-chain transactions. That's what makes CEX trading fast and cheap, and why your on-exchange balance is a claim against the company rather than crypto you directly hold.

That bank comparison isn't just rhetorical. The legacy system a CEX quietly imitates, the commercial banking network, holds close to $19 trillion in customer deposits built up over decades, as the chart below shows. A CEX offers a similar "your balance is a number we maintain" arrangement, but without the deposit insurance and regulatory scaffolding that sit behind those bank figures.

.webp&w=3840&q=75)

Where do the billions in deposits actually live? Most exchanges split customer funds between two very different places:

The takeaway from that split: the vast majority of a well-run exchange's crypto is meant to sit offline, out of a hacker's reach. But "offline" only stops outsiders. As FTX demonstrated, cold storage does nothing to stop the people running the exchange from moving funds themselves.

What Can You Do on a CEX?

A CEX bundles several services into one account. The core is trading: buying crypto with fiat, selling back to fiat, and spot-trading pairs like BTC/USDT or ETH/USD. Around that sit fiat deposits and withdrawals through banks and cards, crypto deposits and withdrawals to external addresses, and order types ranging from simple market orders to advanced conditional ones. Most add mobile apps, customer support, transaction history for recordkeeping, and a broad selection of coins. Many also layer on staking, "earn" accounts, margin, or derivatives, products that carry meaningfully more risk and complexity, and rarely the right place for a beginner to start.

CEX Order Books, Matching Engines, and Liquidity

Most centralized exchanges run on an order book: a live list of every buy order (a bid) and sell order (an ask) for a trading pair. Buyers post what they'll pay, sellers post what they'll accept, and the matching engine continuously pairs compatible orders. When the highest bid meets the lowest ask, a trade executes.

Liquidity ties it together. A deep book, many orders stacked close to the current price, lets you trade sizable amounts without moving the price much, producing a tight spread and little slippage. A thin book does the opposite: a large order walks the price against you. That's why major pairs on big exchanges feel frictionless while obscure tokens can be costly to trade. Market makers, often professional firms, supply much of that liquidity by quoting both sides continuously.

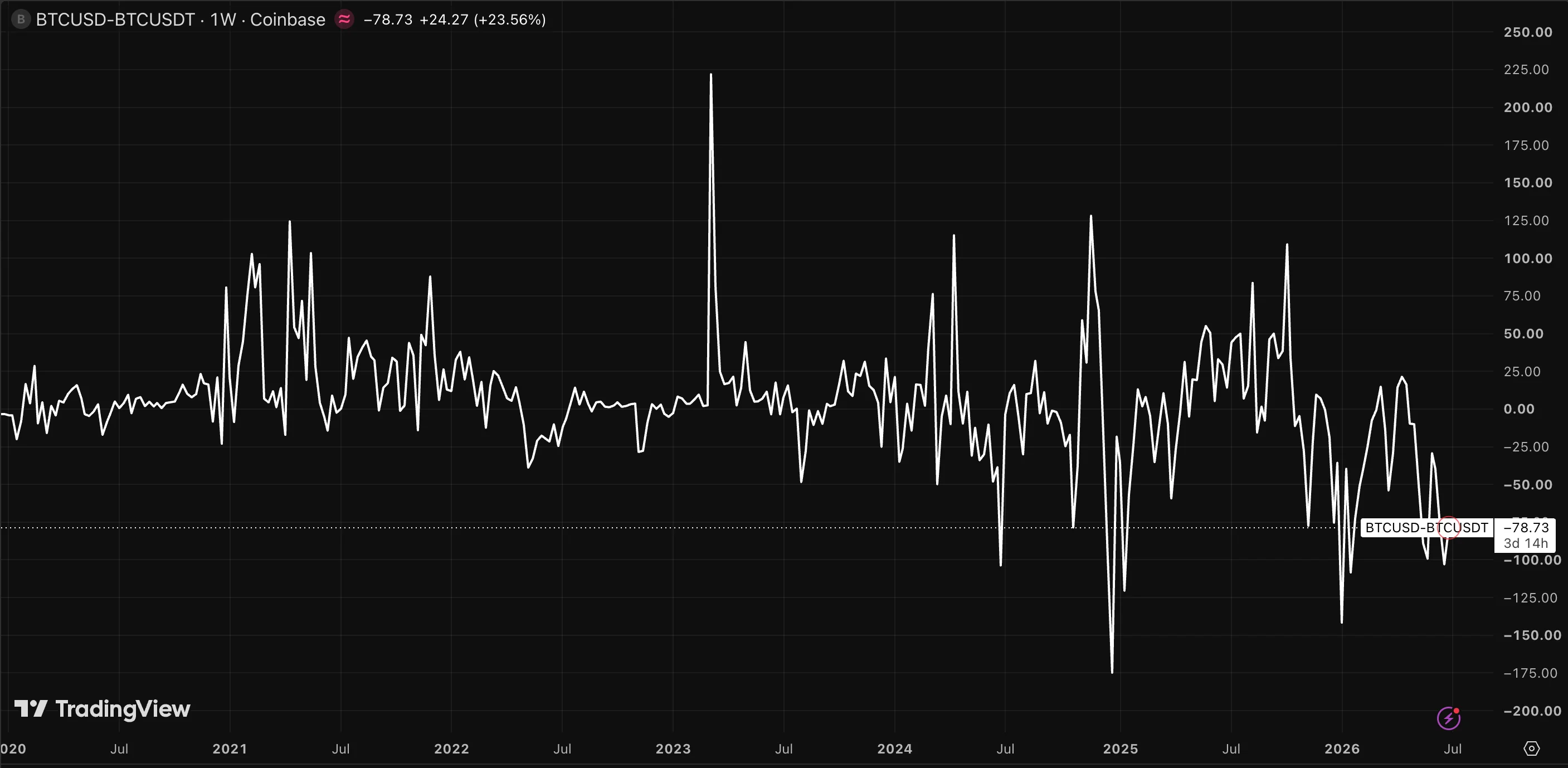

Because each exchange runs its own book, the "price" of an asset can differ between venues and even between pairs on the same venue. The chart below tracks the gap between Bitcoin's dollar price and its USDT price on Coinbase; most of the time it hugs zero, but during volatile stretches it blows out by a hundred dollars or more in either direction. That divergence is the visible footprint of separate order books and uneven liquidity, the same force that widens spreads and slippage on any single venue.

There's an operational wrinkle traders tend to learn the hard way. It's a recurring gripe on r/CryptoCurrency, where one user, watching the market tumble, grew suspicious that the exchange's convenient "maintenance" had less to do with fixing servers than with stopping people from pulling their coins out. Whether it's genuinely overloaded infrastructure or something less flattering, the practical lesson holds: an order already resting on the book can still fill in the chaos, while one you're trying to place mid-outage cannot.

CEX Accounts, Custody, and Private Keys

This is the part most beginners underestimate. On a CEX, you have an account balance, but the exchange controls the actual wallets and private keys behind the scenes. Your balance is the company's promise that the assets are yours; the on-chain coins sit under its control. This arrangement is called custodial, and in plain terms your "Bitcoin" on an exchange is an IOU, a claim on a company that holds the real thing.

Trust like this is exactly what Bitcoin was built to route around. Satoshi Nakamoto's opening framing of the project put the blame on "all the trust that's required to make [conventional currency] work," then pointed out that banks lend deposits out while keeping barely a fraction in reserve. Parking your crypto on a custodial exchange quietly rebuilds the very arrangement Bitcoin set out to escape.

The mantra that captures it comes from educator and Mastering Bitcoin author Andreas Antonopoulos: "Not your keys, not your Bitcoin."

Custody buys real convenience: the exchange can reset your password, recover your account, and spare you from managing keys. It also creates counterparty risk: your access depends on the company staying solvent, secure, and operational. Self-custody flips that, handing you the keys and the entire burden of protecting them. Neither is automatically right; they're opposite positions with opposite failure modes.

The Doomsday Scenario: Where Your Money Stands When Things Fail

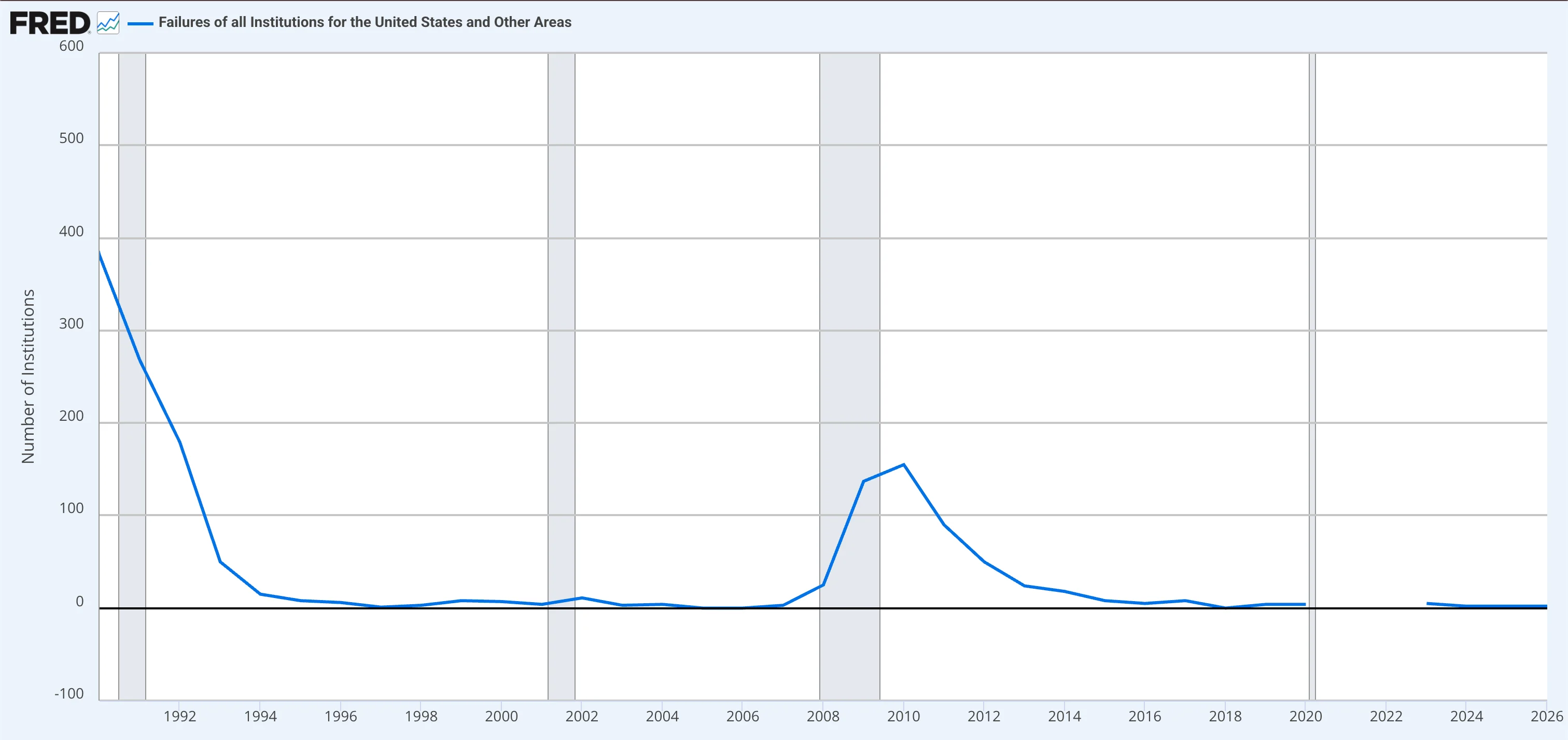

The first column can read like a fantasy of safety, but regulated banks do fail. Hundreds during the early-1990s savings-and-loan crisis and well over a hundred around 2008, as the chart below records. The decisive difference is the outcome: an FDIC-insured depositor is made whole up to the limit, while a collapsed exchange usually converts your balance into a bankruptcy claim.

That last column isn't hypothetical. When QuadrigaCX collapsed in 2019, its founder had died suddenly and was reportedly the only person who knew the passwords to the exchange's cold wallets. Roughly $190 million in customer crypto, sealed off with no "forgot password" button anywhere in sight.

CEX vs DEX: What's the Difference?

A decentralized exchange swaps the company for code. Instead of an account and a custodial balance, you connect a wallet and trade through smart contracts, keeping control of your assets until the instant a trade executes on-chain. The comparison is the cleanest way to see what a CEX is and isn't.

A CEX trades self-custody for convenience: accounts, support, and easy fiat access, at the cost of trusting a company. A DEX trades that convenience for self-custody and on-chain transparency, at the cost of a steeper learning curve and a different risk set. Plenty of people use both. A CEX to move between fiat and crypto, a DEX to trade straight from a wallet.

Centralized Exchange vs Crypto Wallet

A CEX and a wallet get confused because both can "hold" crypto, but they do different jobs. A CEX is a place to trade. A self-custody wallet is a place to control crypto.

The "exchange wallet" address a CEX gives you for deposits adds to the muddle. That address belongs to the exchange's custodial system, not to a wallet whose keys you hold. Moving crypto from a CEX to a self-custody wallet is the step that turns an account balance into something you genuinely own.

Why Do People Use Centralized Exchanges?

Even the people running the biggest CEXs describe them as the on-ramp rather than the destination. Coinbase co-founder Brian Armstrong calls his company a bridge to the cryptoeconomy and steers users toward self-custody. The goal, in his framing, being to make non-custodial wallets so easy that people "don't have to trust us." That's the role in a sentence: a CEX is the doorway in.

Part of the pull is the asset class itself. Measured from the same starting point, crypto's total value has roughly matched the Nasdaq's tech-heavy return over the last three years, but with a far wilder ride, as the benchmark below shows. That mix of big upside and stomach-churning swings is exactly what draws newcomers, and a CEX is the least intimidating way in.

For all the custody caveats, CEXs dominate onboarding for good reasons. They make starting easy: sign up, verify, and buy crypto with a familiar payment method in minutes. They provide the fiat on-ramps and off-ramps that bridge bank money and crypto, which DEXs generally can't offer directly, plus deep liquidity on major pairs, advanced order types, mobile apps, and wide asset selection.

When something breaks, there's support to contact, and the account produces the statements that make taxes and tracking manageable. For beginners especially, a CEX is simply the most practical entry point. The price of that convenience is the cluster of trade-offs (custody, privacy, fees, counterparty risk) that the rest of this guide lays out.

Risks of Using a Centralized Exchange

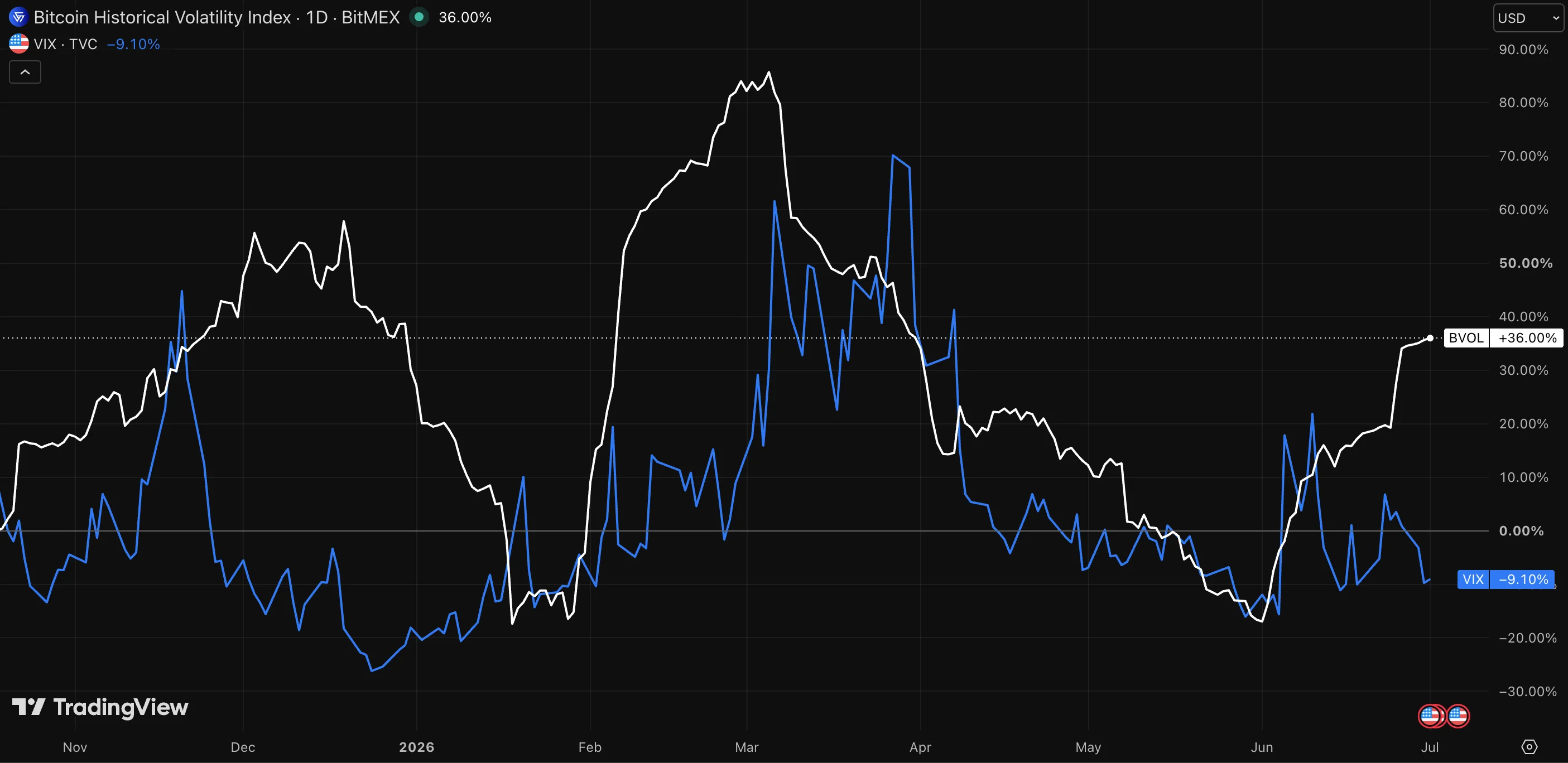

Price volatility is the risk everyone expects. The one that empties accounts is structural: you're trusting a company to hold your assets, stay solvent, and let you leave with them. Price volatility itself is real enough. Bitcoin's volatility gauge typically sits above the VIX, the stock market's "fear index," and swings harder, as the comparison below shows. But it's the structural risk, not the price chart, that turns a bad week into a permanent loss.

Mt. Gox, which began as a site for trading Magic: The Gathering cards before it became the dominant Bitcoin exchange, collapsed in 2014 after losing hundreds of thousands of customers' Bitcoin. FTX imploded in 2022, freezing withdrawals while balances curdled into bankruptcy claims overnight. The common thread is custody: people who had moved holdings into self-custody kept their crypto, while those who left it on the exchange were exposed to the company's failure.

When these companies go under, the legal reality is blunt. Ruling on the 2023 Celsius bankruptcy, Chief U.S. Bankruptcy Judge Martin Glenn found that customers who deposited crypto had effectively handed ownership to Celsius and become "unsecured creditors," last in line behind secured lenders. "Not your keys, not your coins" turns out to describe bankruptcy law as much as it describes a slogan.

The collapses also rhyme. Anyone who lived through Mt. Gox could spot FTX's warning signs from a mile away, one r/BitcoinBeginners commenter noted that the veterans of that earlier, far larger collapse already knew the red flags and had warned others to keep their coins off the exchange. The pattern repeats: fiat withdrawals slow to a crawl, well-connected insiders quietly get their money out, and the CEO takes to social media to swear the funds are fine, often with the crypto-native promise that they're "SAFU."

Remember George Bailey in It's a Wonderful Life, explaining to a panicked crowd that their money isn't in the vault, but out in their neighbors' houses? An exchange only keeps a few percent of funds in its hot wallet for daily withdrawals. When that runs dry during a rush for the exits, the machine goes "down for maintenance," because the money, for that moment, simply isn't there.

Those runs rarely start in a vacuum. They tend to be triggered by broader market stress, the kind captured by the St. Louis Fed's Financial Stress Index, which spiked violently in 2008 and again in 2020, as the chart below shows. When stress like that hits, redemptions surge across the whole system at once, and a thinly reserved exchange is among the first places the strain shows.

That "high yield" red flag has a tell you can check against the real world. In traditional markets, higher yield is compensation for measurable risk: the extra spread investors demand to hold risky high-yield bonds drifts between roughly 3% and 5%, and it widens precisely when danger rises, as the chart below shows. An exchange advertising a flat, "guaranteed" 15% with no visible risk premium is usually funding today's payouts with tomorrow's deposits.

Each blow-up has pushed more coins off exchanges and into cold storage, a structural shift visible on-chain. The practical lesson: treat an exchange as a tool you pass through on the way to somewhere safer.

Proof of Reserves and Exchange Solvency

After the high-profile collapses, many exchanges began publishing proof of reserves to reassure users. It's a genuine improvement that's also widely misread, and the limits matter more than the headline.

Proof of reserves shows that an exchange controls certain assets on-chain, often by publishing wallet addresses or a cryptographic attestation, frequently a Merkle tre, that lets you confirm your balance was counted in the total. What it shows is one side of the ledger: assets held at a single moment.

Solvency depends on both sides. An exchange is solvent only if its assets exceed its liabilities, everything it owes customers and creditors. Kraken co-founder Jesse Powell dismissed the half-measure during the post-FTX scramble: "A Merkle tree of just your assets is purely marketing." Without a matching proof of liabilities, an exchange can flaunt large reserves while owing far more than it holds, or borrow assets briefly to pass the snapshot.

A photo of a full fridge proves nothing if there's a stack of unpaid bills on the counter. Reserve reports are also point-in-time, so they say nothing about the day after, and their scope and method vary.

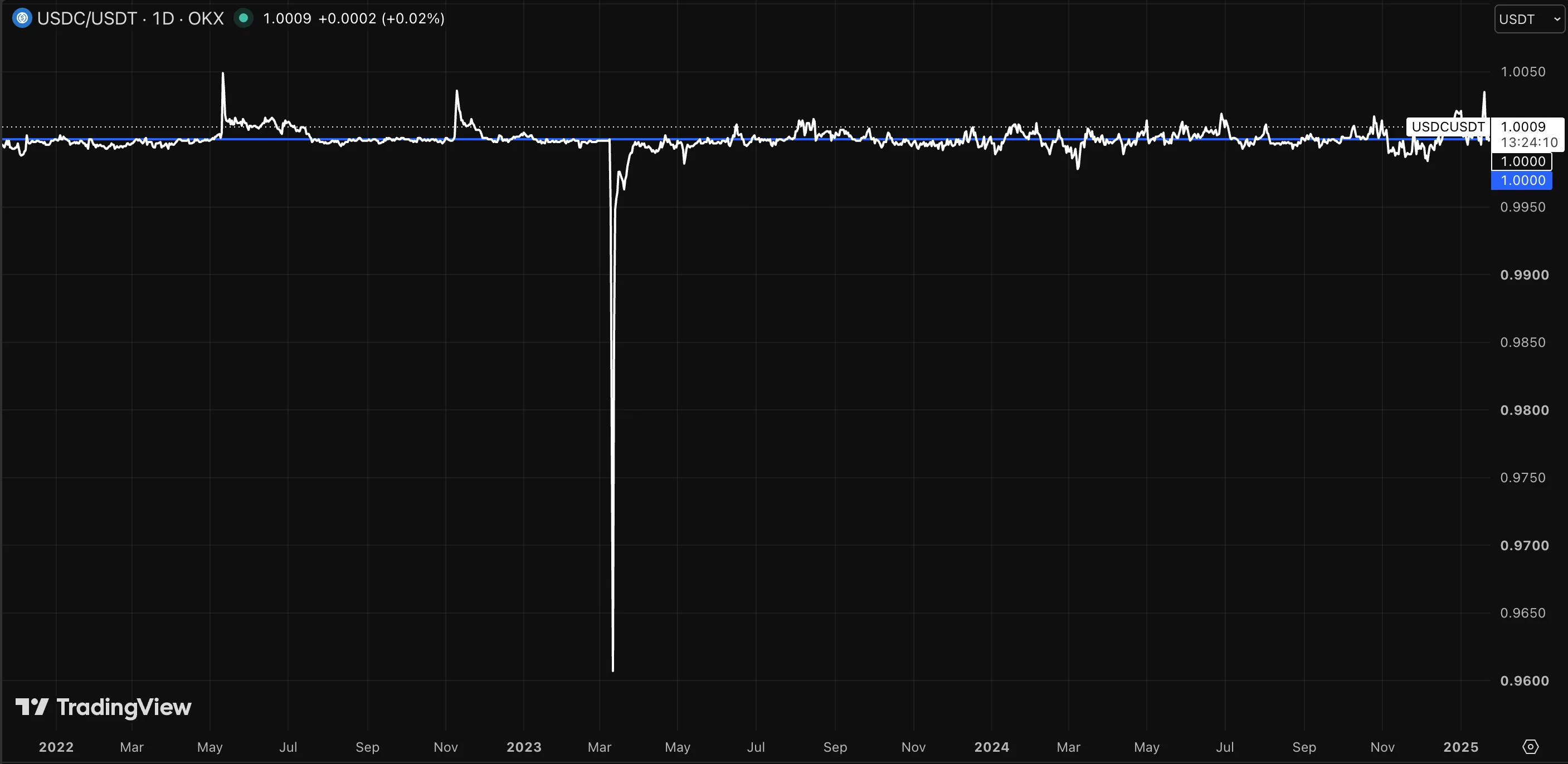

There's a further wrinkle the headline number hides: reserves are only as sound as the assets they're held in. A large share of exchange reserves sits in stablecoins that everyone assumes are worth exactly a dollar, an assumption that has broken before. In March 2023, USDC briefly traded near $0.96 against USDT when one of its banking partners failed, as the chart below shows, before recovering its peg. A reserve snapshot counted at face value can quietly overstate what an exchange really holds when those "dollars" wobble.

A real read on solvency needs both reserves and liabilities, ideally checked by a qualified third party. Proof of reserves is a transparency signal worth having, and a limited one.

CEX Fees: Trading, Deposit, and Withdrawal Costs

Centralized exchanges make money on fees, and the headline trading rate rarely tells the whole story. A common structure charges maker and taker fees (lower for orders that add liquidity to the book, higher for orders that remove it) with several other costs stacked on top.

The big, friendly "buy now" widget on most apps tends to bury its cost in a wide spread rather than a stated commission. A complaint one r/Coinbase user aired at length, arguing that the spread is built so far into the price that even limit orders can't sidestep it, and that hiding the cost this way feels predatory on larger trades. For casual buyers, deposit and withdrawal charges can also dwarf the trading fee. The table below runs one $1,000 purchase two ways to show how much the funding route alone decides your true entry cost.

Anatomy of the CEX Fee Stack (Illustrative $1,000 Purchase)

The numbers are illustrative and vary by platform and network, but the pattern holds: the convenient route can quietly cost around $50 on a single $1,000 buy, most of it before you've traded anything. Comparing the all-in cost (trading fee, spread, and the deposit and withdrawal charges you'll actually incur) is the only fair way to judge.

KYC, AML, and Regulation on Centralized Exchanges

Most centralized exchanges require you to register and verify your identity. This KYC (Know Your Customer) process, paired with AML (Anti-Money Laundering) controls like transaction monitoring, is how CEXs satisfy financial regulations and the demands of the banks and payment providers they rely on. Because a company runs the platform, it can be held to those rules in the jurisdictions where it operates.

Verification usually comes in tiers, and each one trades a little more privacy for a little more access:

The effects cut both ways. KYC unlocks fiat access and the consumer protections of operating inside a regulated system, which many users prefer. It also means handing identifying documents to a company that then stores them, and, as more than one DeFi user has pointed out, a passport scan, a selfie, and a home address sitting on a single server make an inviting honeypot for the next data breach. Requirements differ sharply by country, and crypto regulation keeps shifting, so what's available and what's required depends on where you are and changes over time. A DEX, by contrast, generally uses wallet-based access with no protocol-level identity check, part of its appeal and part of its different risk profile.

How to Use a CEX More Safely

Centralized exchanges make excellent gateways and poor long-term banks. If you're going to use one, enforce a few operational habits.

- Harden your two-factor authentication: Turn off SMS codes, which attackers defeat through SIM-swapping, and lock the account with an authenticator app or a physical security key.

- Send a test transaction first: Before withdrawing your whole stack to a hardware wallet, send a small test amount and confirm it arrives. Yes, you pay the network fee twice. Paying it twice beats firing $10,000 into the void because of a copy-paste error or clipboard-hijacking malware.

- Whitelist your withdrawal addresses: Most exchanges let you pre-approve your own wallet addresses and impose a cooling-off period before new ones can be added. If someone breaches your account, that delay can be the difference between a scare and a loss.

- Kill old API keys: If you ever connected a portfolio tracker or trading bot via an API key, revoke it once you're done. Stale keys are a favorite way for attackers to trade on your behalf without ever touching your password.

- Treat balances as temporary: Once a purchase clears any settlement hold, move long-term savings to a self-custody wallet. Don't let coins you mean to keep sit idle on an exchange.

- Spread your exposure: If you hold meaningful balances, don't stack everything on one platform. Splitting across reputable, regulated venues removes a single point of failure.

Above all six sits one principle: a CEX earns its place as a trading desk and a fiat gateway, but long-term savings belong somewhere you hold the keys.

When to Use a CEX vs DEX vs Wallet

Each tool fits a different job, and experienced users move between all three.

A typical path runs through all three: use a CEX as the fiat on-ramp, trade on a CEX or DEX depending on what you're doing, and move long-term holdings into a self-custody wallet. Knowing which tool you're using, and what you're trusting when you use it, is what keeps your crypto under your control.

Closing Thoughts

A centralized exchange is often the easiest way to enter crypto because it combines account setup, fiat payments, trading, custody, support, and reporting in one platform. That convenience is why CEXs remain the main on-ramp for many beginners and active traders.

The trade-off is trust. When crypto sits on a CEX, the exchange controls the private keys, and your balance is a claim on the platform rather than direct control of the coins. Proof of reserves, regulation, security tools, and reputation can reduce some risk, but they do not remove custody, insolvency, withdrawal, or counterparty risk.

The safest approach is to use centralized exchanges for what they do best: buying, selling, trading, and moving between fiat and crypto. For long-term holding, learn self-custody, withdraw carefully, and treat every exchange balance as temporary rather than permanent storage.